One Stablecoin, Two Worlds

What if the same collateral could power both a stablecoin and a leverage market without constant funding fees or liquidation risk?

Recently, I came across f(x) Protocol, which I found quite interesting and boosting yields over 15% APY in their fxSave product.

The Problem They’re Solving

Stablecoins are all the rage, but they are not all the same. Most are either algorithmic (unstable) or fiat-backed (centralized risk).

f(x) Protocol asks: What if the same collateral could power both a stablecoin and a leverage market without constant funding fees or liquidation risk?

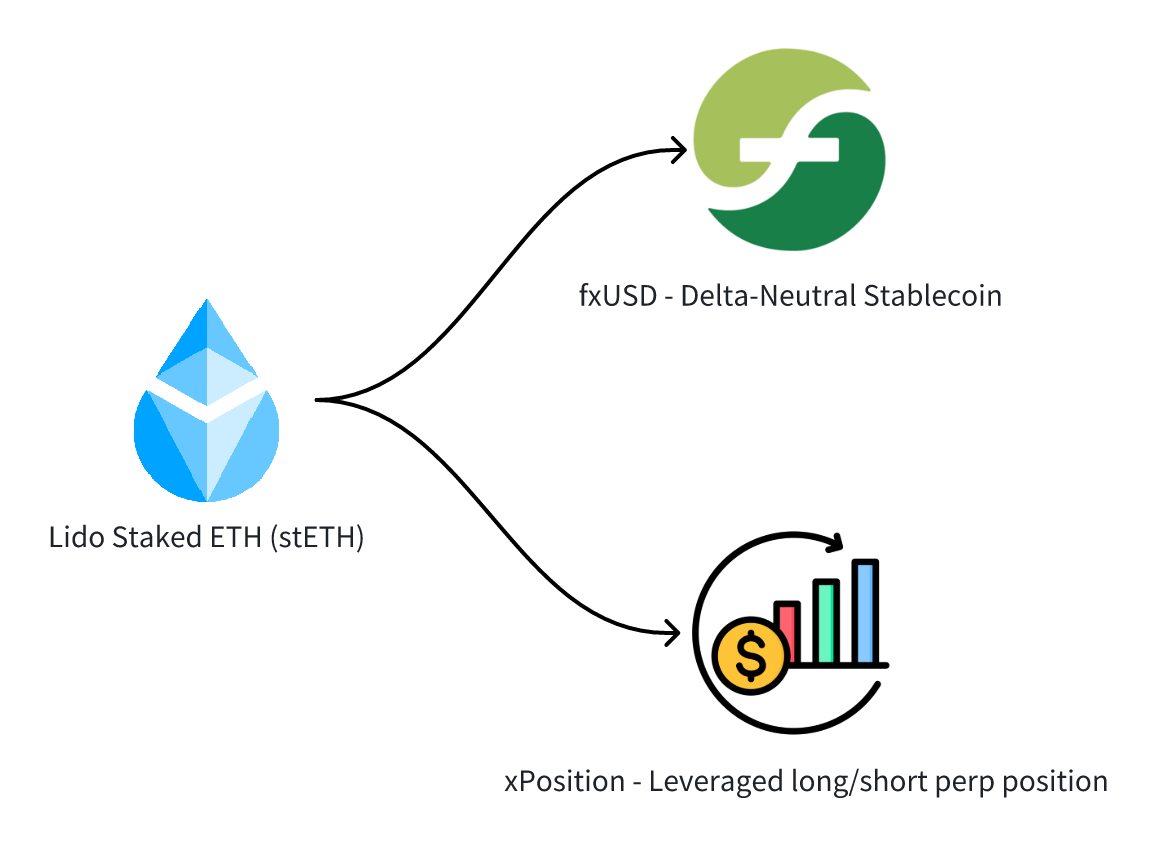

Core Design: Splitting Collateral Into Two Sides

At its core, f(x) takes a yield-bearing asset like Lido staked ETH (stETH) and splits it into:

fxUSD: a delta-neutral stablecoin pegged to $1

xPOSITION fixed-leverage long and/or short positions

Here is the equation governing f(x) Protocol.

n*𝑠 = nf*𝑓 + nx*𝑥

Where:

𝑛 is the number of stETH or WBTC collateral,

𝑠 is the stETH price in USD,

nf is the number of fxUSD,

𝑓 is the fxUSD price in USD,

nx is the number of xPOSITION units, and

𝑥 represents the net asset value (NAV) of xPOSITION in USD

Not Another Terra

fxUSD is not a Terra-style algorithmic coin.

Terra/UST:

Peg relied on a mint-and-burn loop with LUNA (an unbacked token).

When UST slipped below $1, the system printed more LUNA to absorb it.

In a crash, this spiraled into hyperinflation + death spiral, wiping out both UST and LUNA.

fxUSD:

Every single fxUSD is backed 1:1 by stETH or WBTC.

The peg is defended by the Stability Pool.

Risk is tied to underlying collateral, not a circular mint-burn token loop.

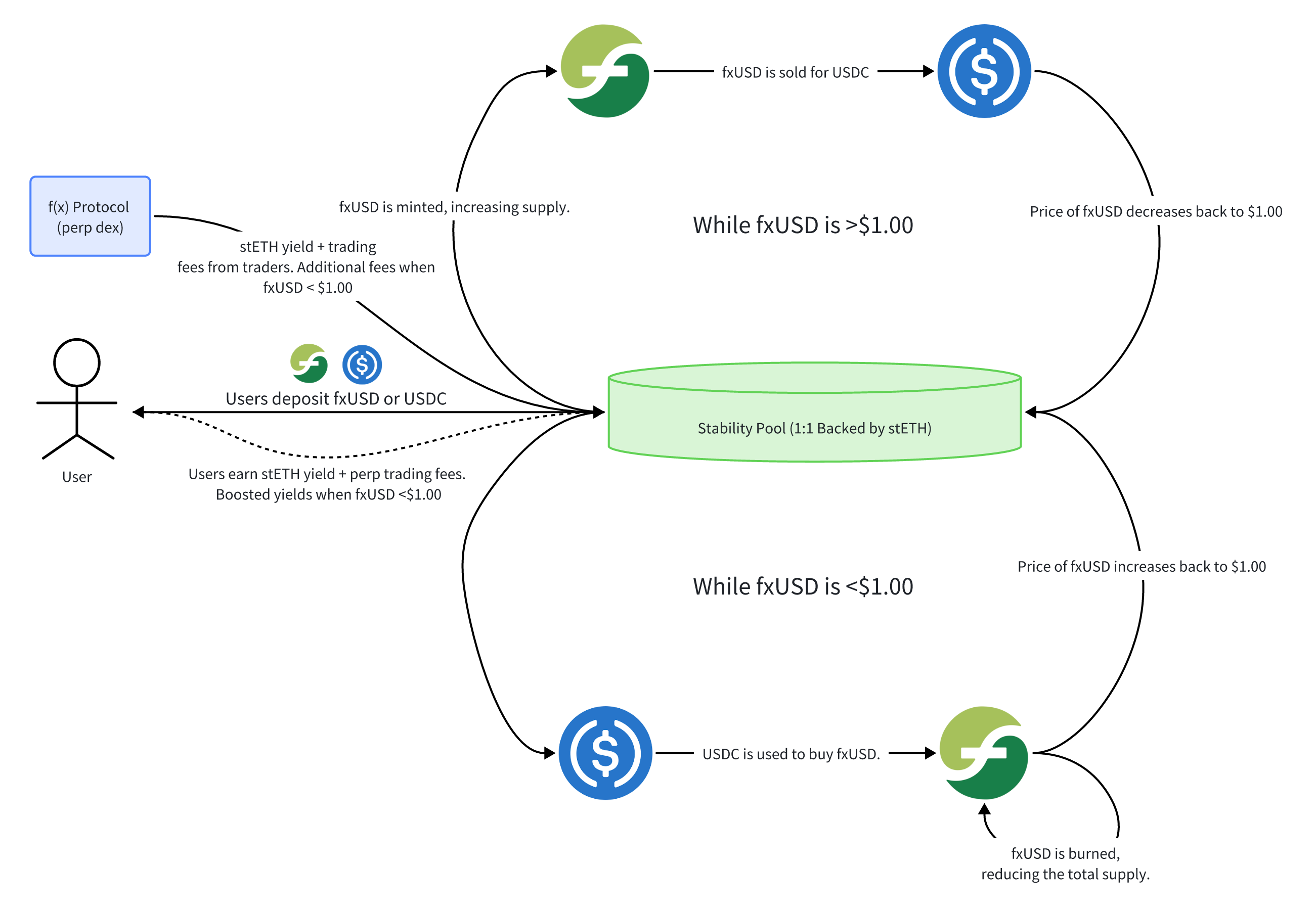

The Peg Mechanism: Why USDC Matters

If fxUSD slips below $1 for too long:

Peg-protection rules take place, preventing users from opening new positions. The system starts charging fees for long positions (who borrowed fxUSD to go long ETH). These fees are routed into the Stability Pool.

With that, USDC in the pool is used to buying up discounted fxUSD (<$1).

Example: You put in 1,000 USDC. If fxUSD drops to $0.98, the system automatically swaps USDC → fxUSD.

That fxUSD is then burned, reducing supply and pushing the price back toward $1.

This is how the Stability Pool both stabilizes the peg and gives instant APY boosts to USDC suppliers.

xPOSITION: Fixed Leverage, No Funding Fees

Its on-chain, permissionless nature means developers can build on its primitives (e.g. integrate fxUSD in other apps or use f(x) for leveraged lending).

Opening a position here feels different than on a typical perp DEX.

xPOSITION = fixed-leverage long/short on ETH/BTC (up to ~10×)

No rolling funding costs eating your PnL

Liquidation is rare due to the “Liquidation Brake,” which rebalances you before you hit the edge of your range.

Liquidation Brake:

Each open xPOSITION has a target leverage range. If market movement pushes leverage beyond a safe threshold, the protocol automatically rebalances the position instead of liquidating.

For xPOSITIONS this means burning a portion of fxUSD debt and using collateral to repay it (thereby reducing leverage). For sPOSITIONS, an equivalent debt is repaid. This operation keeps the user exposed to the asset while bringing LTV back to a safe level, avoiding an all-or-nothing liquidation. Rebalances are typically triggered when a position’s LTV hits ~88% (configurable).

Example:

Let’s say Alice opens a 5x long position (xPOSITION) using stETH.

Starting point:

Alice deposits 1 stETH as collateral (worth $3,000).

She borrows $12,000 fxUSD to go long (so total exposure = $15,000).

Her loan-to-value (LTV) ratio is 80%.

Market moves against Alice

stETH price falls 10% (from $3,000 → $2,700).

Her collateral is now worth $2,700.

Debt ($12,000 fxUSD) stays the same.

New LTV ≈ 88.9% — this is past the safe threshold (88%).

Normally in DeFi, Alice’s entire position might be liquidated instantly (she’d lose most of her collateral).

What f(x) does instead (Liquidation Brake)

Instead of nuking Alice’s position:

The system automatically burns some of Alice’s fxUSD debt using part of her collateral.

Example: Sell a portion of her stETH to repay $500 of debt.

Her outstanding debt goes down to $11,500.

Her LTV falls back to a safer range (say 85%).

Alice still has her long exposure, just slightly smaller, and avoids a total wipeout.

Band System, Liquidation Fallback, Risk Framework:

Positions are bucketed into price “bands” (≈0.15% wide) based on their rebalance trigger. When the asset price moves into a band, all positions in that band are rebalanced together. This batching makes it profitable for keepers (bots) to execute rebalances promptly and efficiently, ensuring the system stays safe.

If rebalancing cannot sufficiently restore collateralization (e.g. an extreme market crash), a position will hit its liquidation line and be closed fully. In liquidation, the remaining debt is burned (for longs) or repaid (for shorts) and the rest of the collateral is seized. The design ensures fxUSD backing is always protected first. Liquidations only occur when a position truly cannot be saved by rebalancing.

The protocol enforces over-collateralization, automatically rebalances positions, and maintains a Reserve Fund (built from fees) to cover any shortfalls. In the unlikely event of systemic insolvency, any remaining bad debt is first absorbed by the Reserve Fund, then (if needed) distributed pro-rata among active leveraged positions. If even that fails, all xPOSITION openings are halted and extreme measures (like converting short collateral via redemption) ensure fxUSD remains 100% backed.

The Stability Pool: USD Delta-Neutral Yield

If leverage isn’t your thing, the Stability Pool is where fxUSD shines for passive earners.

You can deposit:

fxUSD (directly supporting the stablecoin system), or

USDC, which acts like “dry powder” waiting to stabilize the peg.

You earn:

ETH staking yield (from stETH collateral)

Trading fees from leverage users

Lending yield on idle USDC

FXN token emissions

Your position is in dollars (fxUSD or USDC), not ETH. So you’re not exposed to ETH price swings or to traders blowing up their leverage.

In short: if you want safe USD yield without trading leverage yourself, the Stability Pool is the set-and-forget option, and your USDC plays a direct role in keeping fxUSD stable.

Why This Is Different

Most stablecoin protocols and perp DEXs are two separate systems. f(x) fuses them:

Every stETH backs both a stablecoin (fxUSD) and someone’s leveraged position.

The Stability Pool ties the two sides together, ensuring peg stability while generating real yield instead of relying only on token printing.

f(x) stands out by using yield-bearing collateral and rebalancing mechanics, avoiding the unstable dynamics of algorithmic models.

Compared to DAI and GHO, f(x) focuses on yield generation and minimal liquidation rather than just static collateral ratios. Versus crvUSD, f(x) emphasizes a dual-token system (stable + leverage) and stability pool instead of AMM-based liquidations.

In all cases, risks ultimately stem from crypto price crashes and collateral liquidity, but f(x)’s rebalancing and reserve mechanisms aim to keep fxUSD fully backed and close to $1 under most scenarios.

Risk & Safety Nets

No system is risk-free, but f(x) layers defenses:

Automatic rebalancing before liquidation

Reserve fund from protocol revenue

Peg-protection rules

Full 1:1 asset backing, always redeemable

Worst case, fxUSD holders get paid out first.

In a market saturated with either over-engineered algorithmic coins or heavily centralized fiat-backed stables, f(x) delivers something rare: a stablecoin with deep collateral, a clear peg mechanism, and yield powered by real economic activity, all in a single, permissionless system.

If DeFi is maturing into a more sustainable, bank-like infrastructure, f(x) looks like one of the early blueprints.